According to the compensatory theory of tax fairness, people support raising taxes on the rich when they perceive them to have benefited from unequal state action. This idea has been used to explain the historically high top marginal tax rates following the two world wars. In this context, while the poor were risking their lives for their country, many argued that the rich were not sacrificing as much —and some were even benefiting from the war industry. Higher taxes were thus seen as a way to compensate for this unequal treatment by the state and ensure that the war burden was shared more fairly across society.

We use the COVID-19 pandemic to test the compensatory theory in a very different setting.

The pandemic as a massive asymmetric shock

As in the case of the world wars, the pandemic represented a massive asymmetric shock: one that affected all segments of society but to different degrees. While low-income households were more exposed to infection and unemployment, higher-income households were better able to work remotely, and the richest often even increased their wealth. As a result, inequality within countries rose. This raises a key question: Did the pandemic’s unequal impact increase support for taxing the rich?

Compensation and tax fairness

According to standard theories of tax fairness, the pandemic’s unequal effects could increase support for taxing the rich for two reasons. First, under the principle of ability to pay, if the rich become richer, they must pay higher taxes to ensure equal sacrifice. Second, under what we might call deservingness, if the rich have become richer not as a result of their efforts but by profiting from extraordinary circumstances, in other words, from luck, then they are less deserving of those profits and should pay higher taxes.

The compensatory theory provides a more nuanced expectation: what matters is not whether the pandemic had unequal effects but whether those effects were caused by the state. The reason is that an unequal distribution of costs/benefits by the state violates the widely held expectation that it should treat all citizens equally, and if equal treatment is violated, a compensatory intervention—such as higher taxes on those who benefited—is justified to restore it.

Testing the compensatory theory

To test this theory, we conducted an information-provision experiment in the UK with a sample of nearly 4,000 respondents. Participants were randomly assigned to one of three treatment groups (plus a control group that received no information):

- T1: Information about the unequal effects of the pandemic.

- T2: T1 + information highlighting the government’s responsibility for these unequal effects due to lockdown policies.

- T3: T1 + information highlighting the government’s responsibility for these unequal effects due to its failure to impose excess profits taxes.

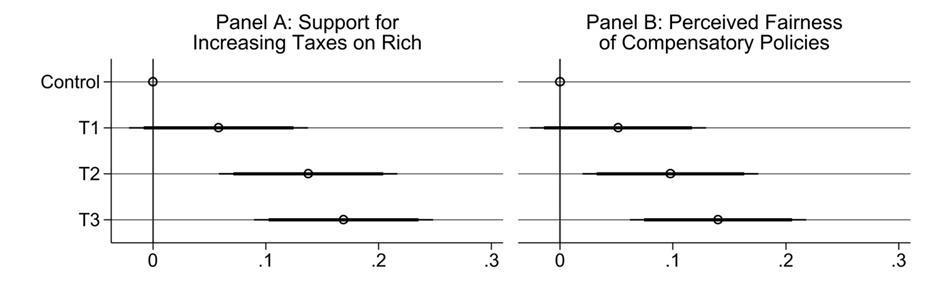

Figure 1: Treatment effects

Note: Outcome in panel A is an ICW index of preferred tax rates and support for different tax reforms. The outcome in panel B is an ICW index of perceived fairness of different policies.

The results, shown in Figure 1, are wholly consistent with the compensatory theory. First, information about the pandemic’s unequal effects (T1) did not increase support for taxing the rich. By contrast, information highlighting the government’s responsibility (either through its actions -T2- or inaction -T3-) did. Second, respondents who received T2 and T3 were more likely to view compensatory policies as fair. Thus, emphasizing the role of the state induced greater support for taxing the rich than inequality created by the pandemic alone, and at least part of this effect is due to the fairness concerns highlighted by the compensatory theory.

When do people support taxing the rich?

People support taxing the rich when it is framed as compensation for unequal benefits granted by the state. This helps explain both why demands to tax the rich increased during the pandemic (see examples here and here) and why they did not materialize. They increased because there was a material basis for compensatory claims, as our findings indicate. However, they likely failed to translate into policy because political elites did not adopt or mobilize these claims, leaving them largely marginal to the overall impact on support for taxing the rich.

Finally, while other arguments for taxing the rich tend to polarize opinion along ideological lines, compensatory claims – because they are rooted in widely shared expectations of equal treatment by the state – appear to generate a wider consensus, even across the political spectrum. The open question is when and why political elites choose to mobilize these arguments.

https://www.journals.uchicago.edu/doi/10.1086/736111

Mariana Alvarado is a Senior Researcher at the University of Geneva

Pablo Querubin is a Professor of Politics and Economics at New York University

Kenneth Scheve is the I.A. O’Shaughnessy Dean of the College of Arts & Letters and Professor of Political Science at the University of Notre Dame

David Stasavage is a Professor of Politics at New York University